Back to Blog

Back to Blog

For some entrepreneurs, the 3 financial statements may seem like busywork best left to an accountant. However, savvy business owners know these numbers tell crucial stories about your business. What these 3 financial statements reveal can significantly impact your cash flow and future, depending on who examines them and the numbers themselves.

The first 3 chapters in your financial story

We’re not talking about just any financial information. We’re talking about 3 financial statements very specifically. Together, the income statement, balance sheet, and cash flow statement give the full picture of how your company is performing financially.

Income statement

An income statement, also known as a Profit & Loss (P&L) statement, shows whether your business is profitable. It details your earnings and expenses over a specific period, revealing if you’re spending more than you’re earning. Many businesses prepare these statements quarterly, yearly, or even monthly to track financial trends consistently.

Balance sheet

Next up is your balance sheet. Like your income statement, this also has another name — the “statement of financial positioning.” It centers on a simple but telling equation to allow you to see your business’s net worth:

Assets = Liabilities + Equity

In contrast to the P&L, your balance sheet looks at a specific moment in time. This is an important difference when you’re thinking about the stories that your accounting documentation tells, especially because circumstances change so rapidly in business. Due to accounts receivable and payable, among other factors, how your finances look on one given day can — and likely will — be very different compared to another even if it’s just a week later.

Cash flow statement

The cash flow statement or “statement of cash flows,” details the cash moving in and out of your business, covering investments, operations, and financing. It’s crucial because poor cash flow management can cause small businesses to fail. Understanding your P&L and balance sheet first is essential, as the cash flow statement integrates and supplements their data with additional insights.

What your financial statements reveal

Your three financial statements together give you a complete picture of how your business is doing. On their own, they’re helpful, but it’s like reading a book without vowels—you can get through it, but it feels incomplete. Together, they reveal the full story, showing you all the crucial details about your company’s financial health and trends. Ensure you understand these statements to get complete insight into your business’s performance.

How well you budget your cash flow

Since cash flow is a big component of all three of your statements, you’d likely expect that you can gather a lot about your business’s cash flow when you look at all of them. What can you especially see? If you’re good with that cash. As we mentioned before, this is a major part of your company’s likelihood of survival.

Among the things those evaluating your cash position will be able to see are:

- If you keep consistent — and right-sized — reserves.

- If you tend to hedge for emergencies or lean on financing often.

- If you experience — and anticipate seasonal — fluctuation in revenues.

- If and when you invest your cash, and how it affects your ability to pay your outstanding bills.

- If you correctly manage your trade credit relationships.

How you manage your working capital

You have money to put into your business? That’s great news. Working capital is a huge sticking point for lots of small-to-medium businesses who need access to more funds to initiate growth phases. Many businesses seek financing specifically for working capital, so it’s important to know if you’re using your own productively.

Your financial statements will reveal a lot, including:

- If you’re keeping too much working capital on hand instead of investing it.

- If, on the other hand, you’re investing too much and not keeping enough in reserves.

- If your investments are incorrectly distributed to accelerate growth.

- If you’ve put too many resources into one asset class versus another preventing maximum return on investment (ROI).

If you’re making the money you could — or should — be

Whether or not your business is maximizing its revenues can end up being a subjective conversation. There are a few things about the conversation, though, that aren’t a matter of opinion. Or, at a minimum, are less debatable than others.

Your statements will shed light on:

- If your profit margins are too slim, and, relatedly if your cost of goods (COGS) is too high.

- If your raw materials are increasing faster than you’re raising your prices or getting better terms with suppliers to sustain your margins.

- If you’ve created a sustainable monthly recurring revenue (MRR) model.

- If you’re pricing similarly to others in your sector — and making the same margins.

- If your fixed and variable costs are on target or should be adjusted so you can net more profit.

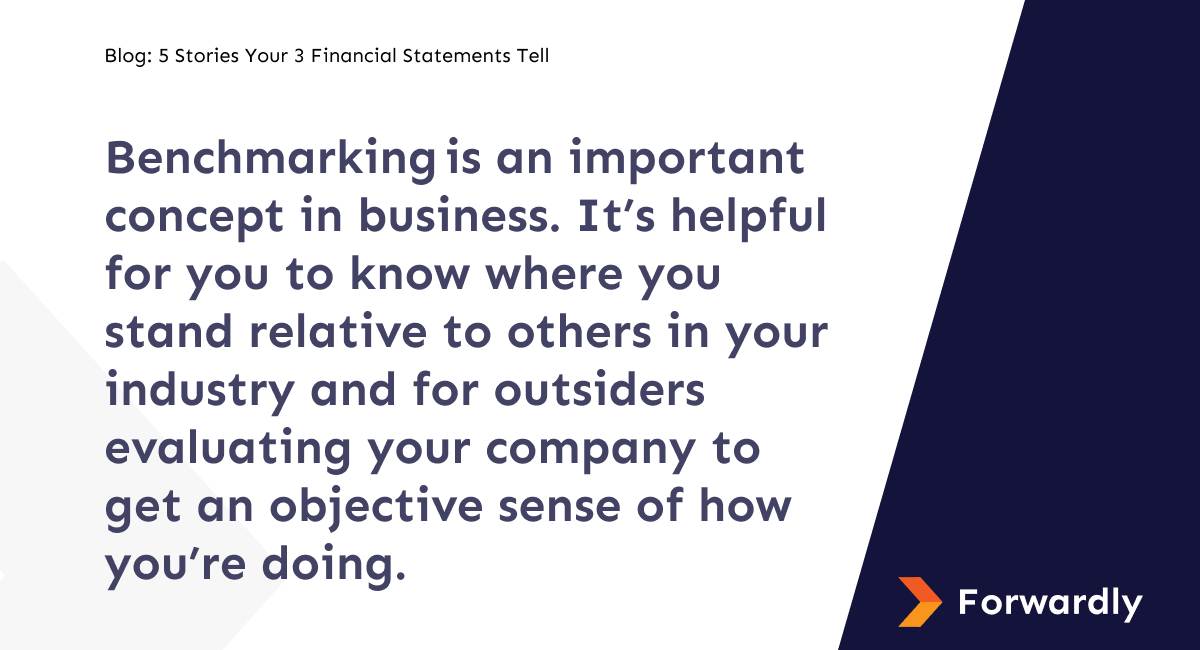

Where do you fall relative to industry peers

Benchmarking is an important concept in business. It’s helpful for you to know where you stand relative to others in your industry and for outsiders evaluating your company to get an objective sense of how you’re doing. It also allows industry experts to be able to map you in your competitive landscape.

Your financial statements will help with benchmarking by:

- If you’re growing are the same rate as comparable companies.

- If current economic conditions are impacting you differently than your peers.

- If you’re allocating your capital in substantially different ways, or your operating costs are relatively significantly higher or lower.

- If you’ll hit profitability before other major competitors.

If your capital asks are realistic

There comes a point in the life cycle of many SMBs when you’ll want to borrow money. It’s not a badge of shame — far from it. Many entrepreneurs look for business financing when they want to accelerate their growth or seize an opportunity. And no amount of savvy cash flow management or diligent recordkeeping can see the future.

If you’re asking for a loan or an investment, your statements will be able to expand on:

- If you have the cash flow to be able to pay back a lender in the case of a loan.

- If you have consistent revenue history that makes you a good candidate for a term loan.

- If you’re in a hyper-growth stage, or your business is on the decline.

- If you already have a lot of outstanding debt.

- If you don’t have enough equity left to offer.

The bottom line

Understanding and analyzing your 3 financial statements isn’t just about keeping the books straight—it’s about making smart, informed decisions for your business. Your income statement, balance sheet, and cash flow statement each tell a unique part of your business’s financial story. By keeping a close eye on these statements, you can stay on track, make strategic adjustments when needed, and show potential investors or lenders why your business is worth their time and money. Getting a handle on your financials means you’re better equipped to guide your business toward lasting success and profitability.