Back to Blog

Back to Blog

If you’ve ever had to make a last-minute payment, you’ve probably wondered: Are wire transfers immediate? The short answer? Sometimes. The long answer? It depends on where you’re sending money, what time of day it is, and how much patience you have. Let’s break it down in a way that makes sense for small business owners who don’t have time to wait around for funds to clear.

How fast are wire transfers, really?

Wire transfers are frequently touted as “instant,” while the reality is more like “fast, but not always instant.” Here’s why.

- Domestic wire transfers (inside the U.S.) are often handled within a few hours and can arrive the same business day if sent before the bank’s cutoff period (generally around 2-5 PM EST).

- International wire transfers can take anywhere from one to five business days, depending on currency conversion, intermediary banks, and country-specific regulations.

According to the Federal Reserve, the average wire transfer completion time in the U.S. is about 24 hours, not exactly instant, but much faster than regular ACH transfers, which can take 2-3 business days.

Why aren’t wire transfers always immediate?

Banks and financial organisations don’t use magic; instead, they use secure payment networks such as Fedwire, Clearing House Interbank Payments System (CHIPS), and Society for Worldwide Interbank Financial Telecommunication (SWIFT) but not designed for instant transactions. Here’s what can slow things down:

- Bank cut-off times: Banks process wire transfers only during specific hours, often ending between 2 PM and 5 PM EST. If you miss the deadline, your transfer won’t go through until the next business day.

- Weekends & holidays: Banks typically don’t process wire transfers on weekends or holidays. For example, if you transmit a wire on Friday evening, it will not begin to move until Monday morning.

- Fraud prevention checks: Banks conduct security screenings on high-value transfers to prevent fraud and money laundering. These checks can add extra processing time before your funds are approved for release.

- Intermediary banks: If your transfer involves multiple banks (especially for international wires), it might pass through several financial institutions before reaching the recipient. Each step adds processing time.

- Receiving bank processing times: Just because your bank sends the wire doesn’t mean the recipient’s bank will process it immediately. Some banks take extra time to clear incoming wires, especially for large amounts or new accounts.

Can you speed up wire transfers?

If you’re looking for faster payments, wire transfers may not always be your best bet. Forwardly offers real-time payments (RTP), which can move money in seconds, 24/7. That means instant payments, even on weekends and holidays, without worrying about cut-off times.

Also read: How Faster Payment Tech Leaves Money Wire Transfers in the Dust

Wire transfer checklist: What to have ready

Before you send a wire transfer, make sure you have all the necessary details. Missing or incorrect information can lead to delays or failed transactions. Here’s what you typically need:

- Recipient’s full name and address: Ensure it matches their bank records.

- Recipient’s bank name and address: This helps in routing the transfer correctly.

- Bank account number: Double-check this to avoid sending money to the wrong account.

- ABA routing number (for domestic transfers): Identifies the recipient’s bank in the U.S.

- SWIFT/BIC code (for international transfers): Used to process international wire transfers.

- Transfer amount and currency: Confirm the exact amount and currency type to avoid conversion issues.

- Purpose of payment: Some banks require a reason for the transfer to prevent fraud.

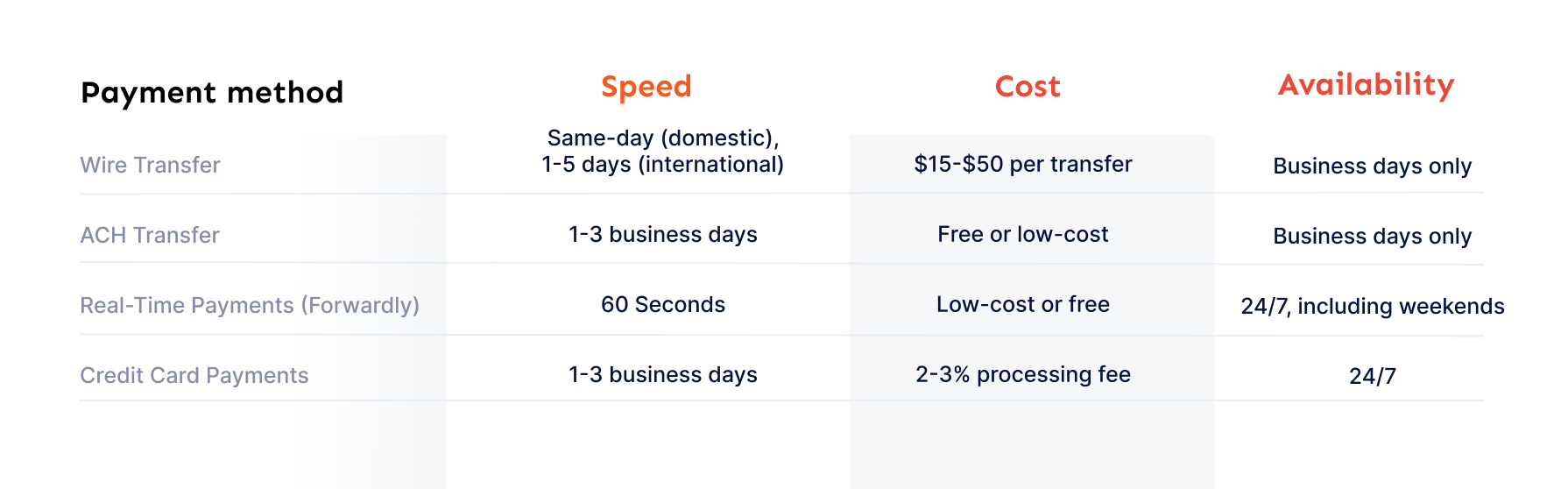

Wire transfers vs. other payment methods

Small business owners need to weigh their options when it comes to sending or receiving payments. Let’s compare:

Are wire transfers worth it for small businesses?

If you’re making large payments and need a secure method, wire transfers work well but they’re not the best for everyday transactions. The high fees and processing times make them less ideal for frequent business payments, payroll, or vendor payments.

Instead, small businesses should look into faster, lower-cost options like real-time payments with Forwardly, which eliminate waiting times and cut transaction costs because we bet you won’t enjoy watching your money take a scenic route before it lands where it needs to go.

At the end of the day, cash flow is king, and no one wants to wait longer than necessary to get paid. Because let’s be real; your business runs on cash, not on “pending” transactions.